The 65% figure is not a single tax rate. It is the combined share of all government taxes and levies in the final pump price for petrol, often reaching 59 to 65% depending on the exact wholesale price, for diesel.

Article 40 and others protect personal rights

The Irish Constitution (Bunreacht na hÉireann) explicitly allows the state to impose taxes “for the purposes of the common good.” Article 40 and others protect personal rights, property, livelihood, etc, but these rights are not absolute, they are supposed to be balanced against the needs of society, public services, infrastructure, and policy goals like climate targets.

Courts have consistently held that taxation is a core sovereign power of the Oireachtas, but not an arbitrary seizure.

For the Common Good

The “Common Good” Argument vs Reality

The Constitution allows taxation “for the purposes of the common good”. Governments and courts interpret this broadly to include:

- Climate policy, carbon tax revenue is supposed to fund retrofitting, fuel allowances, and “just transition” measures though critics note underspending and poor ring-fencing in practice.

- Public services, infrastructure, welfare, etc.

However, when a large and growing share of taxpayer revenue funds asylum accommodation, with an average nightly cost of €71 per person and daily spending of €3.29 million in 2025, and millions being sent to other countries, many citizens reasonably ask: Is this really serving the “common good” for Irish taxpayers, or is it a policy that ignores the struggles of working people facing high fuel, housing, and living costs?

Secondly, when some politicians and those connected to the political system are reportedly profiting millions from this spending, it further undermines the government’s credibility when it demands such high taxes from ordinary citizens.

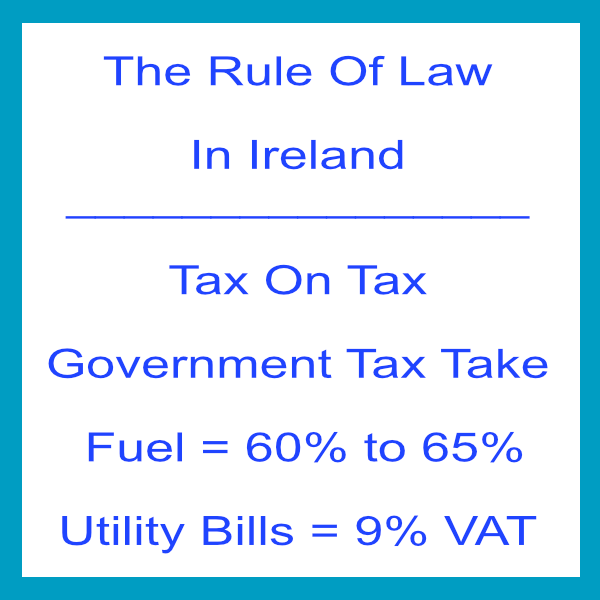

Tax On Tax – Double Taxation

VAT is charged on a price that already includes excise duty and carbon tax.

The state layers excise + carbon tax + 23% VAT on the taxes often pushing the government take to 60–65%.

This is the classic “tax on tax” sometimes called “cascading tax“, that many people find particularly irritating with fuel in Ireland.

How It Works in Practice – April 2026, with temporary cuts in effect until 31 May – The pump price builds up like this:

- Base cost -The wholesale/refinery cost of the actual fuel, this fluctuates with global oil prices.

- Non-carbon excise duty (Mineral Oil Tax non-carbon part) — Fixed per litre. Currently reduced temporarily: 42c on petrol (after 15c cut), 26c on diesel (after 20c cut). Without the temporary cut it would be higher (57c petrol / 46c diesel).

- Carbon tax – €71 per tonne of CO₂ → roughly 16.4c per litre on petrol and 19c per litre on diesel.

- Small levies — NORA levy (currently paused/suspended until end of May, normally 2c) + any other minor charges.

- VAT at 23% Applied to the total of steps 1–4 (base + all the above taxes and levies).

These figures are only for information purposes and may change in accordance with pricing and charging trends.

Because VAT is calculated on the already-taxed amount, you end up paying 23% VAT on the excise duty and carbon tax themselves. This inflates the final price and increases the government’s overall take.

Real World Impact on the 60–65% Figure.

With current pump prices (roughly €1.85–€2.10 for petrol and €2.00–€2.25+ for diesel in April 2026), taxes and levies (including the VAT stacking effect) typically account for:

- 60% on diesel

- Up to 65% on petrol (especially when the pre-tax oil price is lower)

The excise duty remains the single biggest chunk, but the VAT-on-tax mechanism meaningfully boosts the total government share. Critics rightly point out this makes fuel taxation more burdensome than a simple flat rate would suggest.

Legal & Policy Justification

- EU law requires that VAT be charged on the full taxable amount, which includes excise duties and similar charges (such as carbon tax).

- Irish law follows this exactly via the Value-Added Tax Consolidation Act.

- Governments defend it as standard practice for consumption taxes, while critics call it an hidden way to maximise revenue from essentials like fuel.

It really feels like a form of hidden theft.

In short:

Tax-on-tax occurs because VAT is a percentage tax applied to a price that has already been inflated by excise duty and carbon tax. This stacking effect increases the overall burden on consumers and boosts government revenue from every litre sold.

It is morally unfair – “theft by another name“.

Current Reality in Ireland

With the temporary excise cuts (15c on petrol, 20c on diesel + NORA levy pause) still in effect until 31 May 2026, taxes and levies still make up roughly 55–65% of the pump price on petrol and around 55–60% on diesel, depending on the exact wholesale price that day.

The tax-on-tax (VAT at 23% or the temporary reduced rate on energy) is applied to a base that already includes excise duty and the carbon tax (€71 per tonne of CO₂, adding ~16–19c per litre). This cascading effect means the state extracts more revenue than a simple flat tax would.

Governments of different parties have repeatedly voted this structure into law through annual Finance Acts.

Morally unfair and disproportionate

- Fuel is an essential for work, family life, farming, and haulage in a country with poor public transport outside cities. Taking 60%+ of the price via compulsory levies feels like punishment for needing to drive.

- The regressive impact hits harder on middle and lower incomes, rural households, and small businesses as a share of their spending.

- The carbon tax component is meant to change behaviour, but many see little visible return: e.g. better infrastructure or alternatives while costs rise year after year toward €100/tonne by 2030.

When politicians maintain or increase these rates and the cascading mechanism, despite public anger, it can feel like extraction for revenue and ideology rather than genuine necessity.

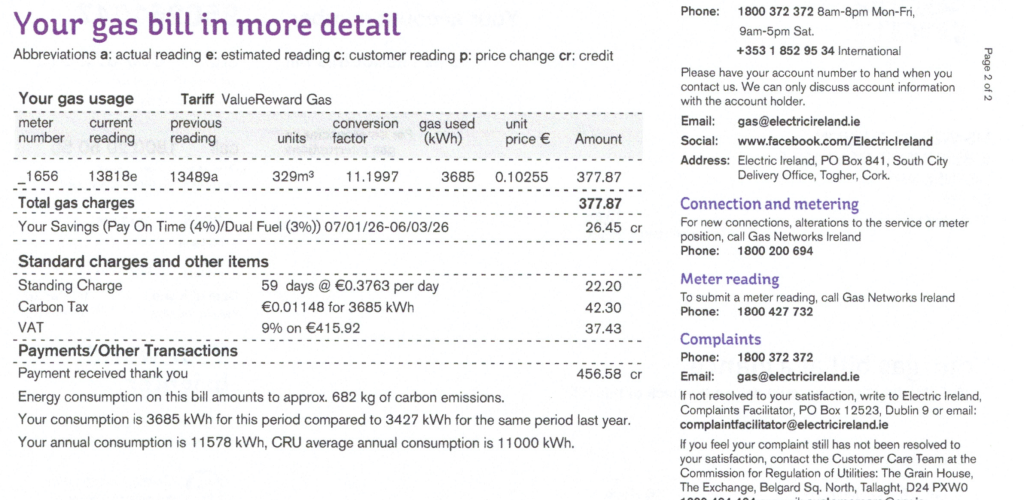

Do you know you are paying Carbon tax on your utilities bills.

Bill Summary

Difference (VAT + any other charges): €78.71

Net amount (before VAT): €377.87

Total amount due (including charges/VAT): €456.58

Carbon Tax: €42.30 + 9% VAT = €46.10

Tax On Tax

Similar Pattern of Double Taxation

The same “tax-on-tax” logic applies to electricity and gas bills:

- Bills include wholesale energy costs + network charges + public service obligation (PSO) levies + carbon-related costs.

- VAT at 9% (reduced rate, extended until 31 December 2030) is then charged on the full bill total.

You are effectively paying VAT on the levies and charges already embedded in the bill.

This is another form of cascading taxation, though at a lower VAT rate than fuel.

Households bear most of this VAT because businesses can often reclaim it.